Mortgage life insurance cover ensures your family doesn’t need to worry about repaying the mortgage if you die.

For most families, monthly mortgage payments are their largest outgoing. A mortgage protection policy can repay the remaining mortgage balance if you die.

Find Your Cheapest Mortgage Life Insurance Quote. Please Complete The Form Below

Do you really need Life Insurance for your Mortgage?

Without Life Cover for your Mortgage, your family’s home could be at risk.

If the worst happens to you, it could mean the family is forced to sell their home unless they have another means of repaying the mortgage balance (or the mortgage is small enough to be covered by the remaining partner’s income).

Remember that with one income gone forever, the amount of a new mortgage that could be applied for would be greatly reduced.

Perhaps even to the point where it becomes impossible to purchase a new home.

A Life Insurance policy to cover your mortgage helps to make sure that, if the worst happens, your loved ones are protected, and the family home is theirs.

With no more mortgage payments, the family’s monthly outgoings will also be significantly reduced.

Click To Compare QuotesThink twice before buying Life Insurance through your bank or mortgage lender

In our view, it may end up costing more than you realise. Lenders, without telling the customer, add their own markup of up to 50% to the price available elsewhere.

Even going directly to the insurer will, bizarrely, sometimes end up costing policyholders far more.

What if you repay your mortgage early?

The simple answer is that you’re free to do what you like.

- The life insurance policy runs independently of the mortgage. You do not need to keep a mortgage to maintain the life insurance policy.

- On the other hand, if you’re sure you no longer wish to keep the policy, you can terminate it at any time. The insurance company will not charge you any penalty if you cancel the plan.

Some brokers may charge a penalty if you cancel your policy, but Chimat does not.

If you already have a death in service benefit from your employer, do you still need Life Cover for your Mortgage?

It’s an option, but not necessarily the best one.

You may have sufficient life cover through your employer’s scheme to repay the mortgage. But before deciding to go down this route, you should consider the following:

- If you use the lump sum death benefit to pay off your mortgage, will your family be left with sufficient income to manage?

- If you change your employment during the mortgage, you will lose the death-in-service benefit. How will your mortgage be covered then?

- If you apply for life cover at that point, it will probably be more expensive because you’ll be older.

However, if you have a health condition or develop one before applying for life insurance, it could further increase the cost of your cover. In some cases, it may even become impossible to find.

So relying on your employer’s death in service benefits as a means of covering your mortgage could still leave your family at risk if your circumstances change.

The safest option is to have a separate life insurance policy for your mortgage, providing guaranteed coverage regardless of future changes in your health or employment.

There are two types of Life Cover policies normally used to cover mortgages, each with important differences

Level Life Insurance for your mortgage

With this type of cover, the amount of the claim payable remains fixed throughout the policy.

Normally, this type of plan should be used for interest-only mortgages. However, there is no reason why you can’t have this type of cover for a repayment mortgage.

Decreasing Life Insurance for your mortgage

This is the type of policy designed specifically for repayment mortgages (where you pay the lender both capital and interest each month).

The amount of cover starts at the full mortgage amount and declines over the mortgage term.

The reason it falls is that as you repay the mortgage each month, the total amount owed to the lender decreases.

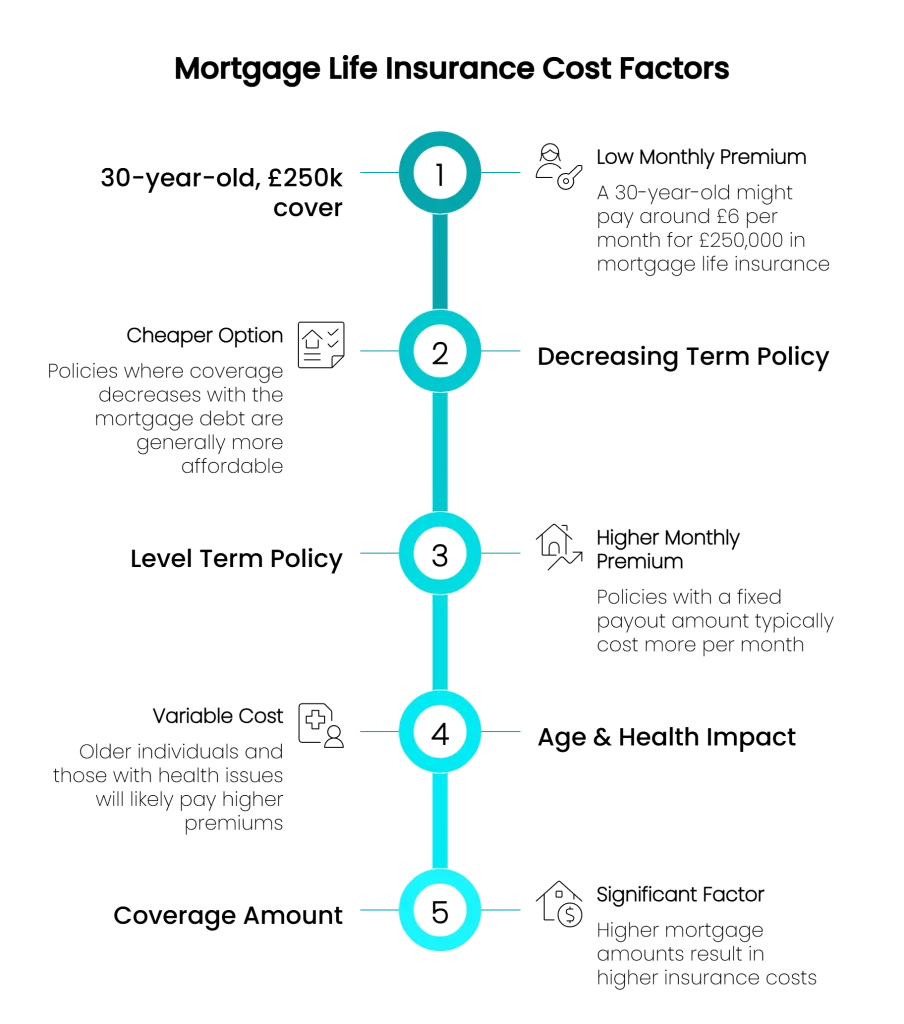

How much could Life Cover for your Mortgage cost?

The example premiums below are based on non-smoker rates and were sourced on 15th January 2026. The term for all of these policies was over 25 years.

Individual cover – monthly premium examples:

| Age | Policy Type | Cover Amount | Monthly Premium |

|---|---|---|---|

| 35 | Decreasing Life Cover | £150,000 | £7.06 |

| 35 | Decreasing Life or Critical Illness | £150,000 | £33.30 |

| 45 | Decreasing Life Cover | £150,000 | £13.78 |

| 45 | Decreasing Life or Critical Illness | £150,000 | £77.17 |

Joint cover – monthly premium examples:

| Age | Policy Type | Cover Amount | Monthly Premium |

|---|---|---|---|

| 35 | Decreasing Life Cover | £150,000 | £11.38 |

| 35 | Decreasing Life or Critical Illness | £150,000 | £60.00 |

| 45 | Decreasing Life Cover | £150,000 | £24.09 |

| 45 | Decreasing Life or Critical Illness | £150,000 | £140.56 |

The above example premiums are for illustration purposes only. Any terms offered would be subject to underwriting.

If you have any health conditions, take a look at the Life Insurance for people with Health Conditions section.

Sources and related information:

- https://www.lloydsbank.com/life-insurance/help-and-guidance/do-you-need-life-insurance-for-a-mortgage.html

- https://www.postoffice.co.uk/life-cover/guides/mortgage

Paul has over 12 years of life insurance expertise. Renowned for his dedication and approachable nature, he’s a trusted advisor committed to helping clients secure their future.